Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Last Updated on: 19th March 2025, 11:58 pm

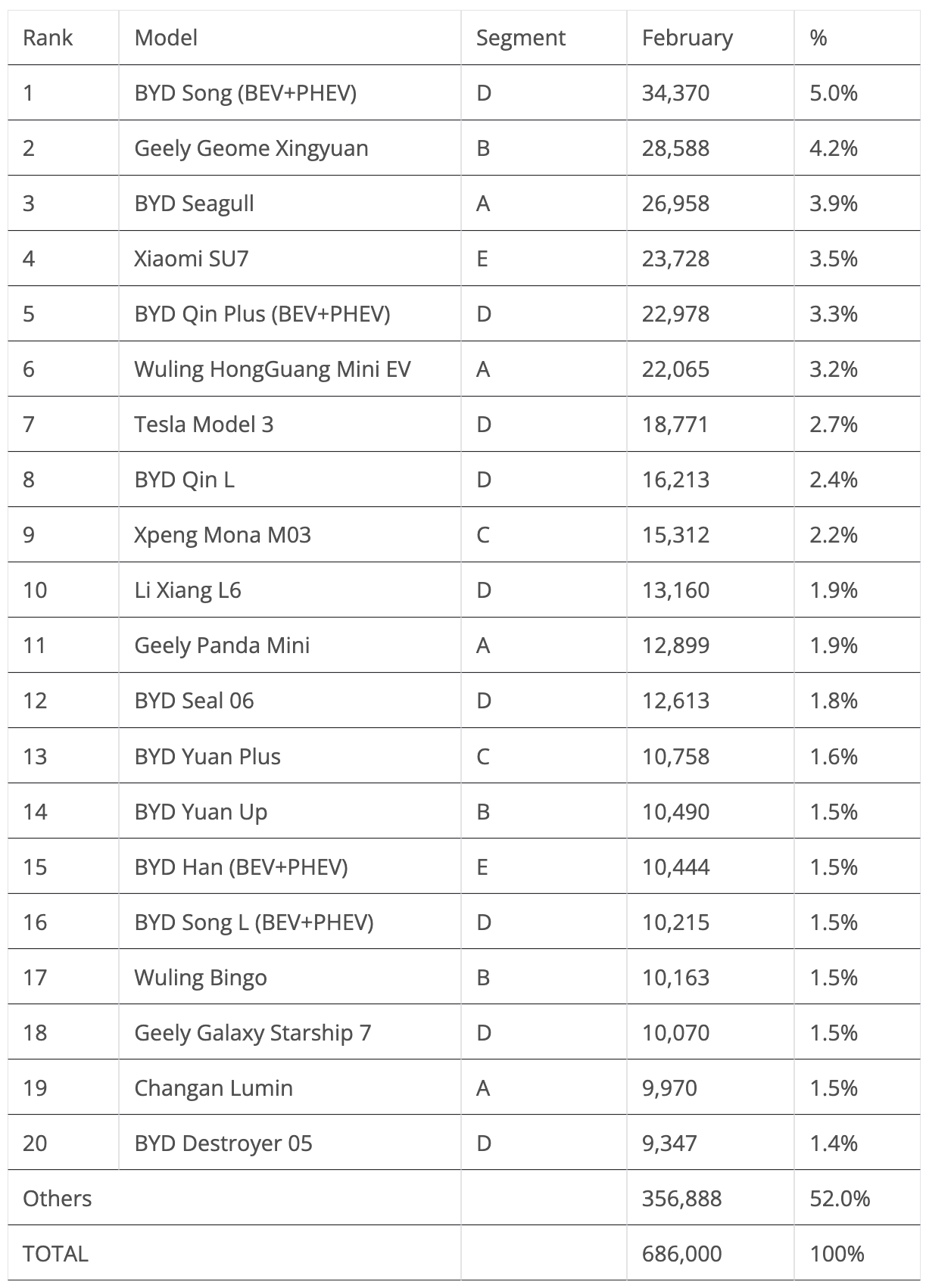

Plugin vehicles are all the rage in the Chinese auto market, even in one of the slowest months of the year — due to the Chinese New Year celebrations — with plugins scoring 686,000 sales (in a 1.39-million-unit overall market).

Looking deeper at the numbers, BEVs were the fastest growing technology, going up by 94% to 427,000 units, while PHEVs grew 83% and EREVs by 12%.

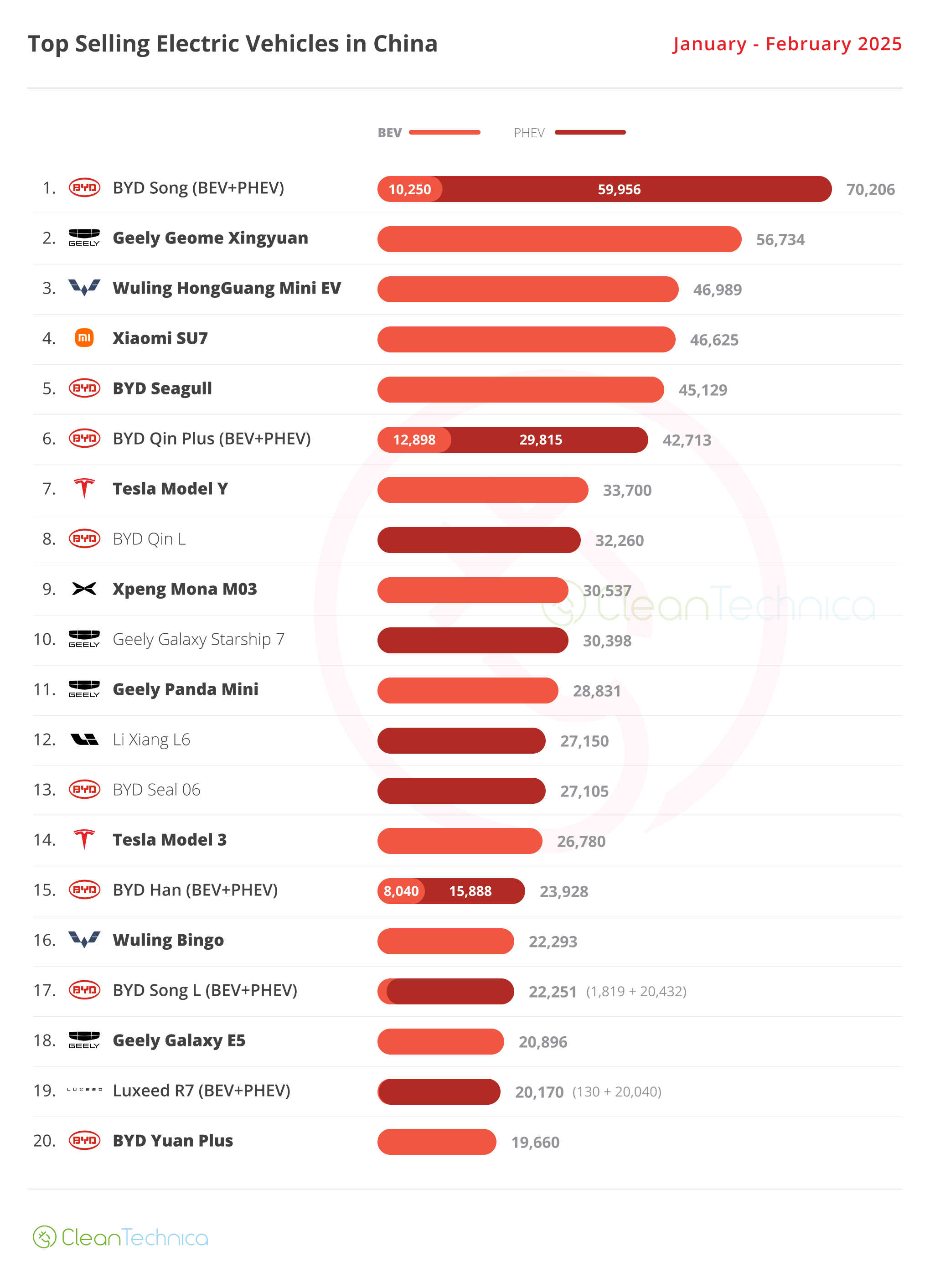

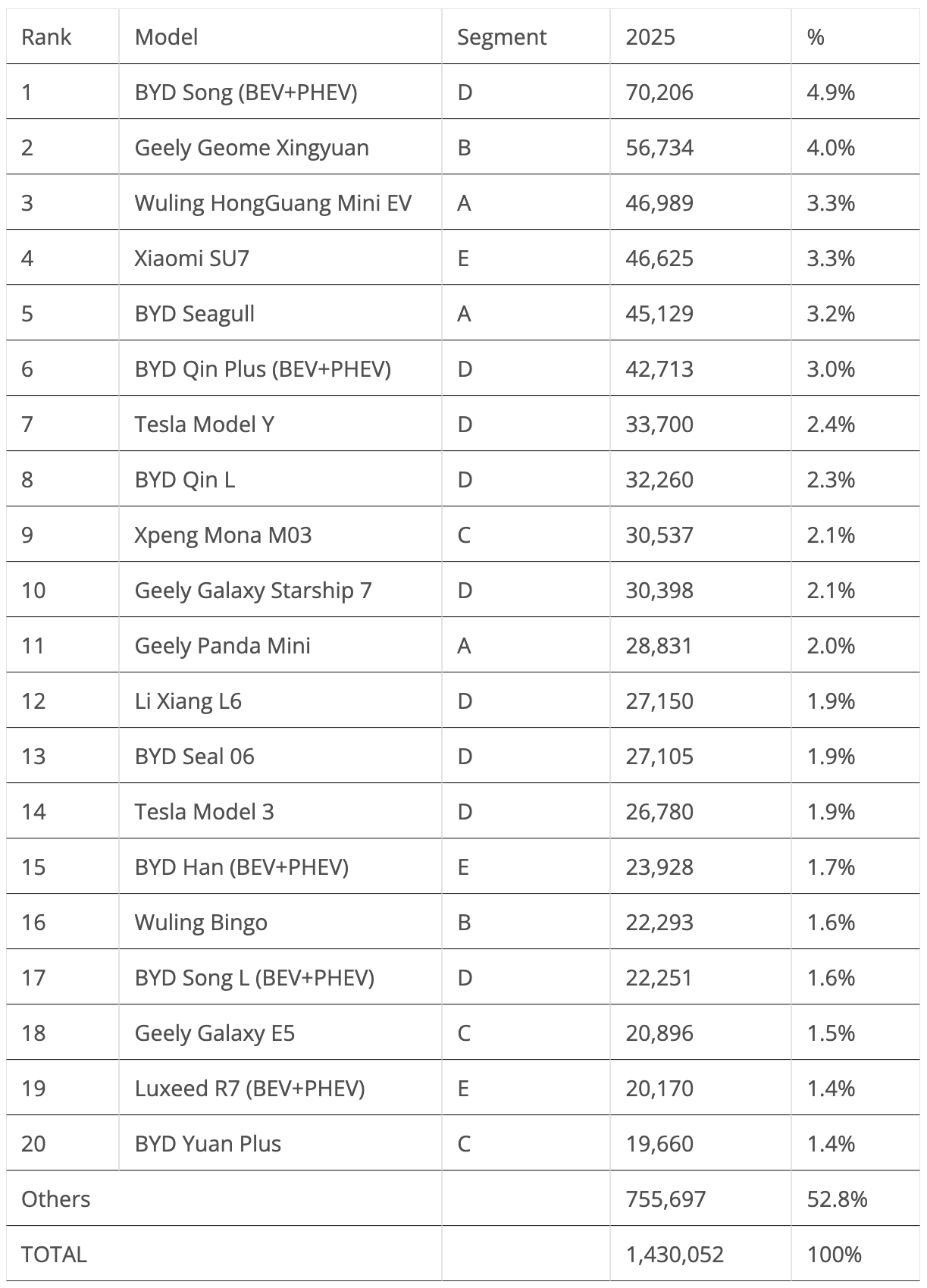

This pulls the year-to-date (YTD) tally to over 1.4 million units, and with March set to be another strong month, we should see Q1 end at over 2 million units.

Share-wise, February saw plugin vehicles hit 50% market share! This is a full 15 percentage point result above where we were 12 months ago. Full electrics (BEVs) alone accounted for 31% of the country’s auto sales, also a stark departure from the 22% score of February 2024.

This pulled the 2025 share to 45% (in the same period last year, it was at 33% share). BEVs alone jumped to 27% (20% BEV in Jan–Feb ’24), and considering that the last month of the quarter is usually a strong month, we can assume that the country’s plugin vehicle market share will end close to the 50% mark in Q1, and the first half of the year should see it above 50%.

(Could China finish the year close to 66%?)

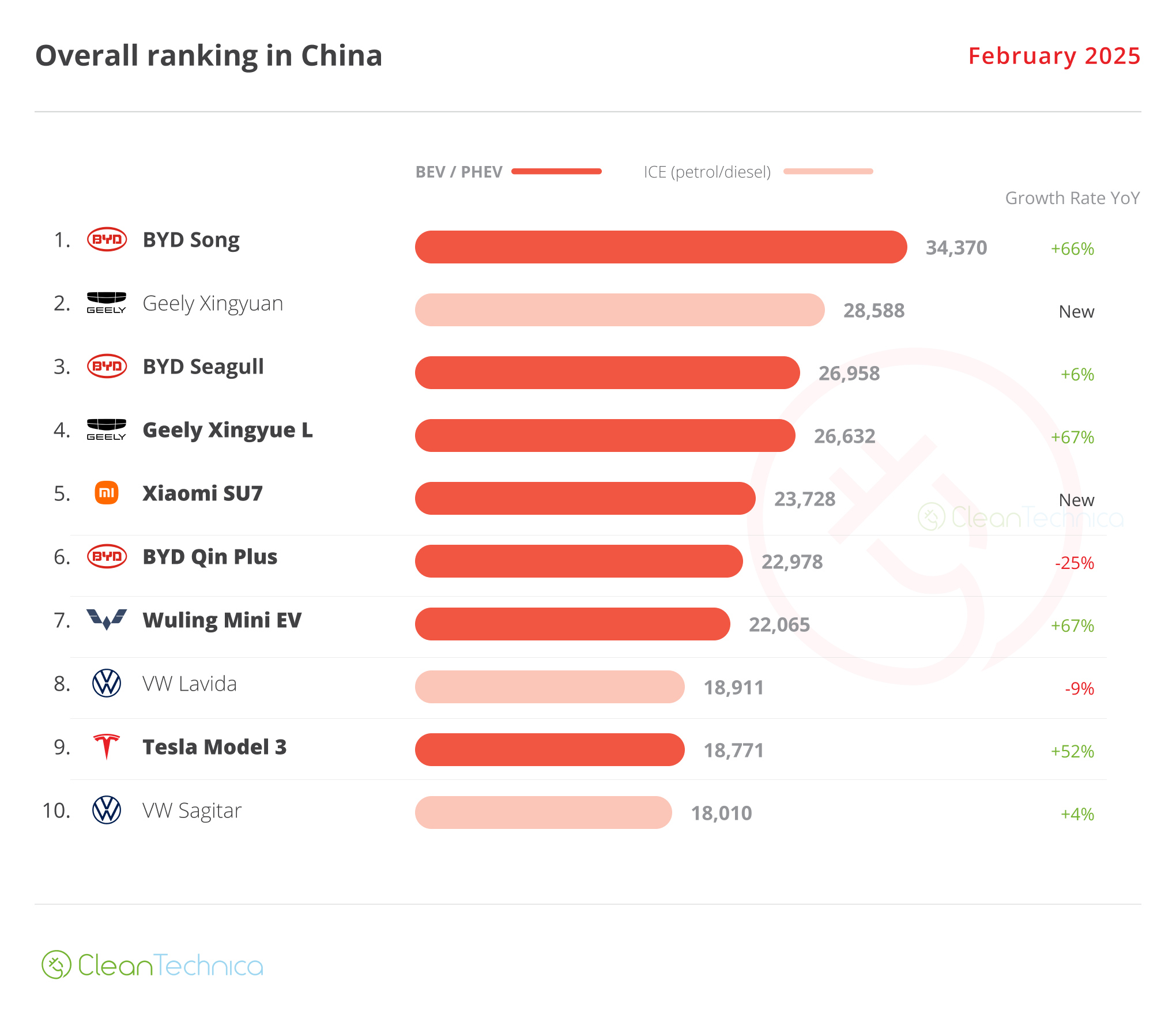

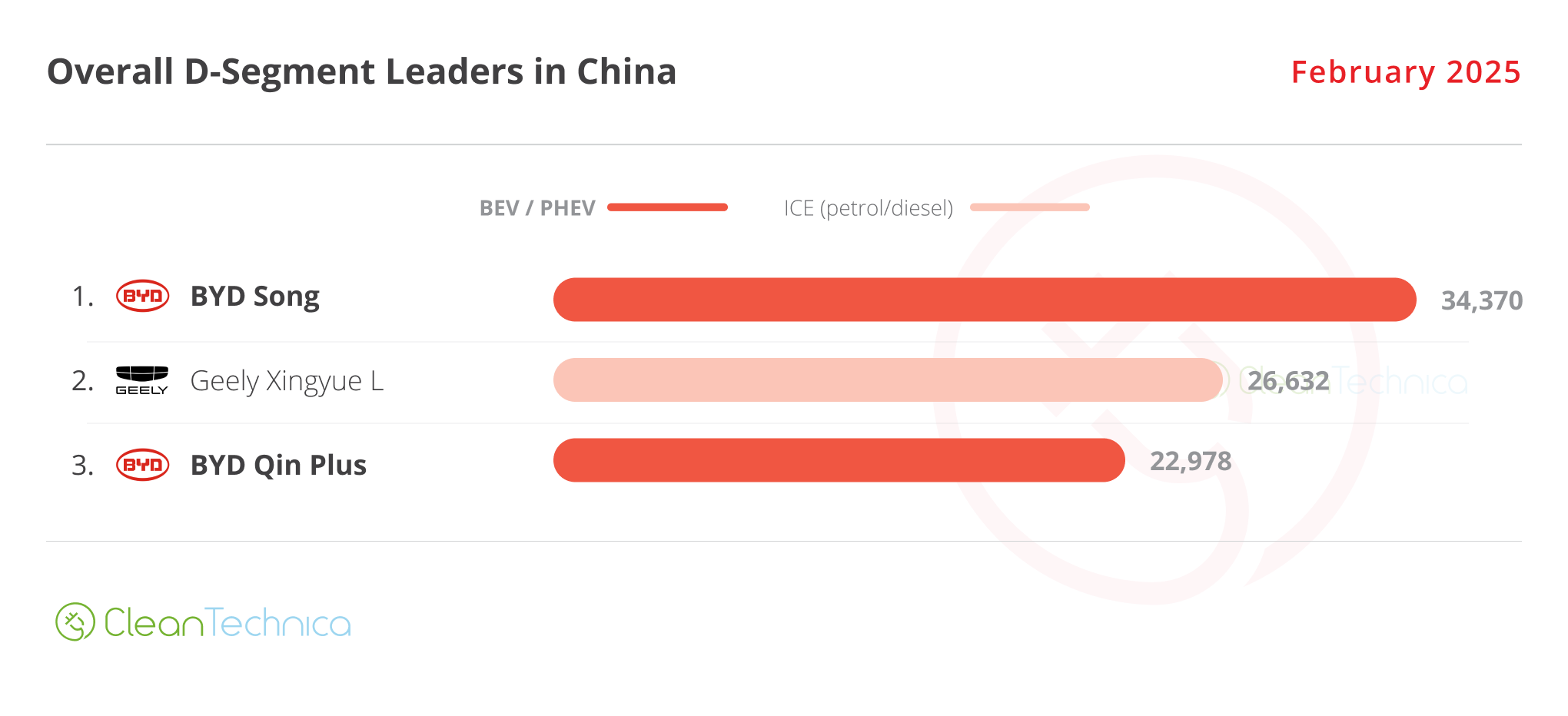

In the overall ranking, as usual, the beginning of the year had ICE models populating the top positions, but not as much as expected. Whereas a year ago ICE models had six models in the top 10, this time there were only three. The BYD Song was the usual best seller, but behind it, Geely continued to impress, with the small Xinguyan winning silver. They were followed by the BYD Seagull in the last place on the podium, and the Geely Xingyue L ICE midsize SUV (also known as Geely Tugella and Renault Grand Koleos in export markets) ended in 4th.

So, the top four positions were divided between BYD and Geely. A sign of the future?

Funny enough, while there was the usual representative from Tesla in the top 10, this time it wasn’t the Tesla Model Y, now in the middle of a refresh cycle, but instead the Model 3. That was thanks to an outstanding 18,771 registrations. As a result, it managed to win a top 10 spot, 9th, its highest standing in China since 2022.

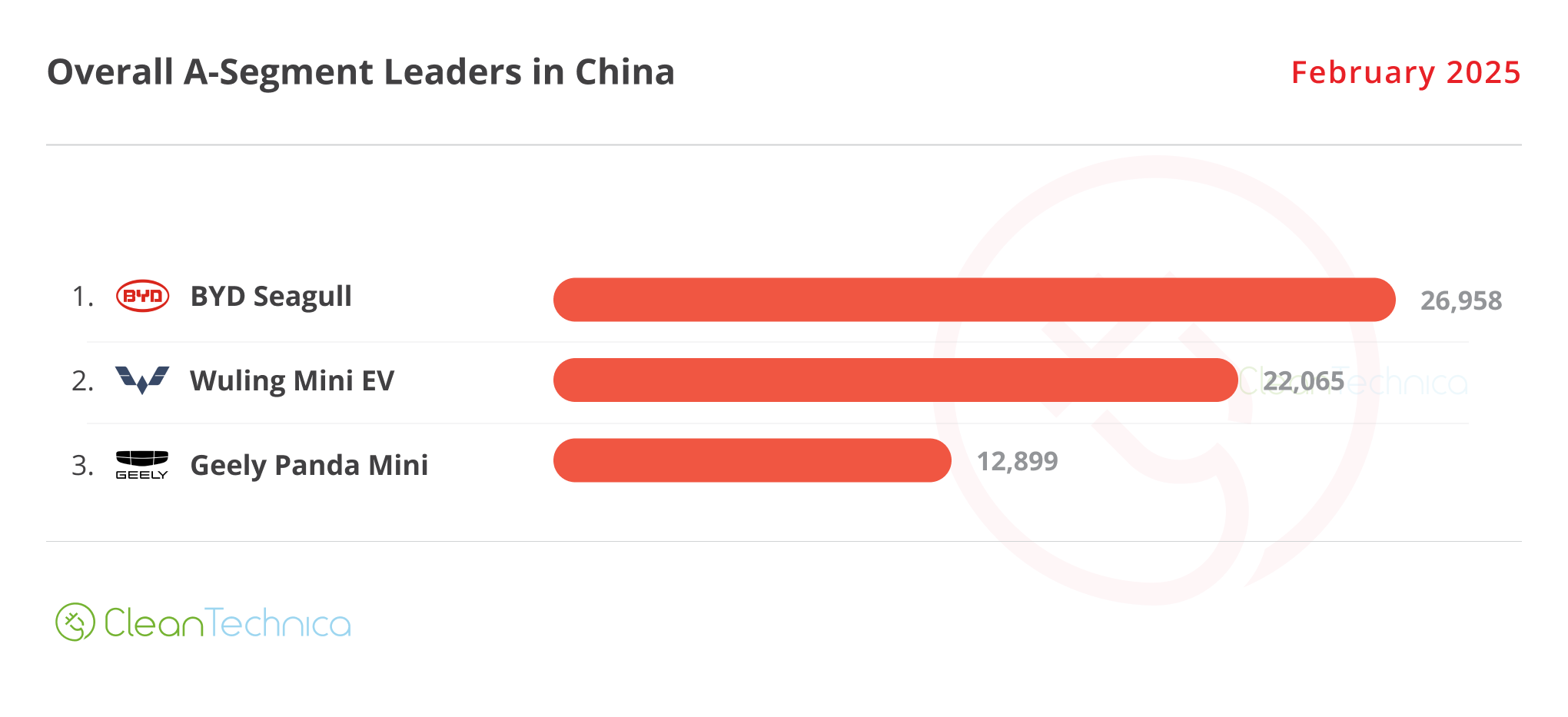

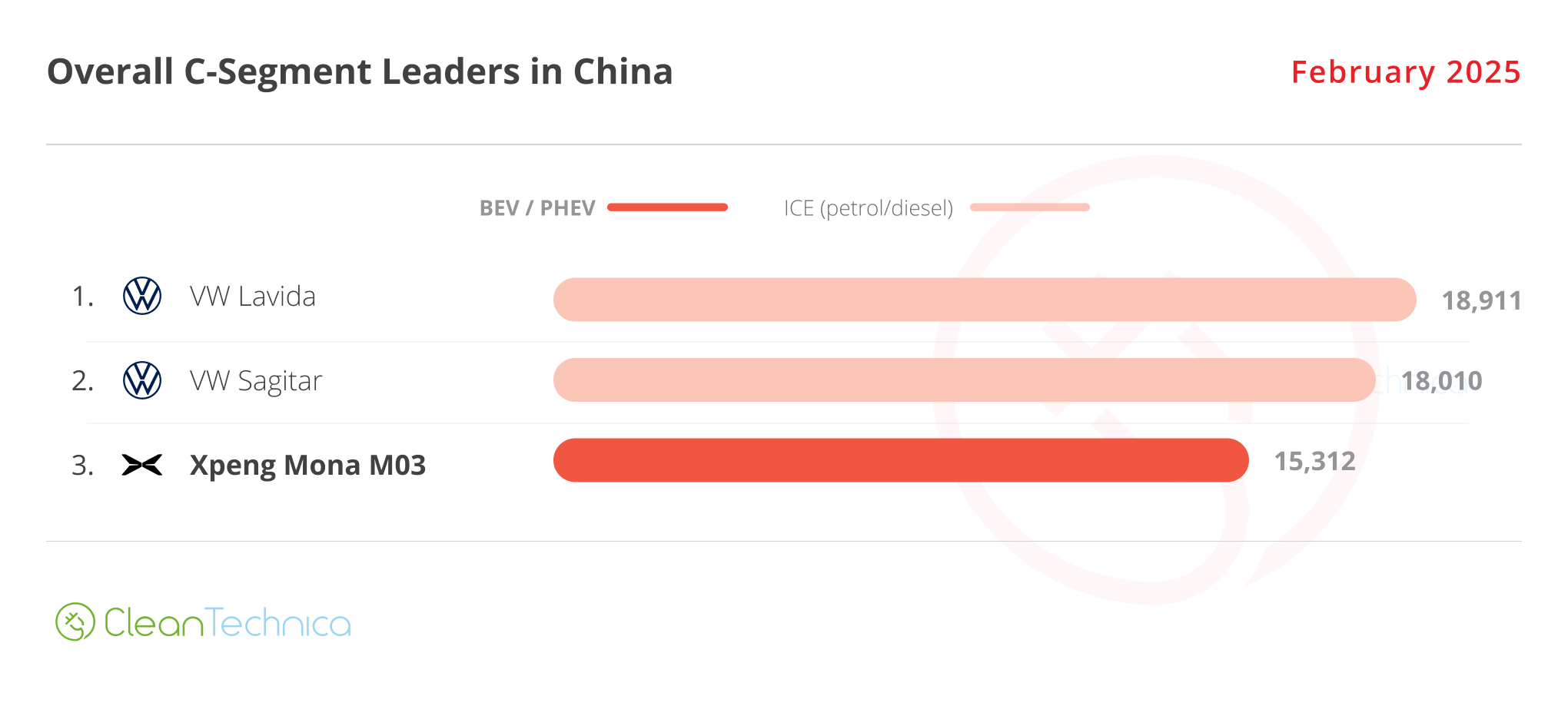

Looking at the best sellers in several size categories, all but the C segment (compact cars) have plugins leading the way. In fact, the C segment was the only category where ICE managed to place two representatives, while in all other categories, they were the minority. This is a recurring topic, as it seems that the C segment is the hardest of all to convert into EVs. Looking at the bright side of this, it means that models like the Xpeng Mona M03 and Geely Galaxy E5 have plenty of room to grow….

The biggest surprise was Geely getting the #1 and #2 spots in the B segment, thanks to the little Geely Xingyuan taking the trophy and its ICE crossover Binyue taking the runner up spot.

It was a great month for Geely, which placed four representatives on category podiums, second only to BYD (5 representatives). Am I starting to see a trend here?…

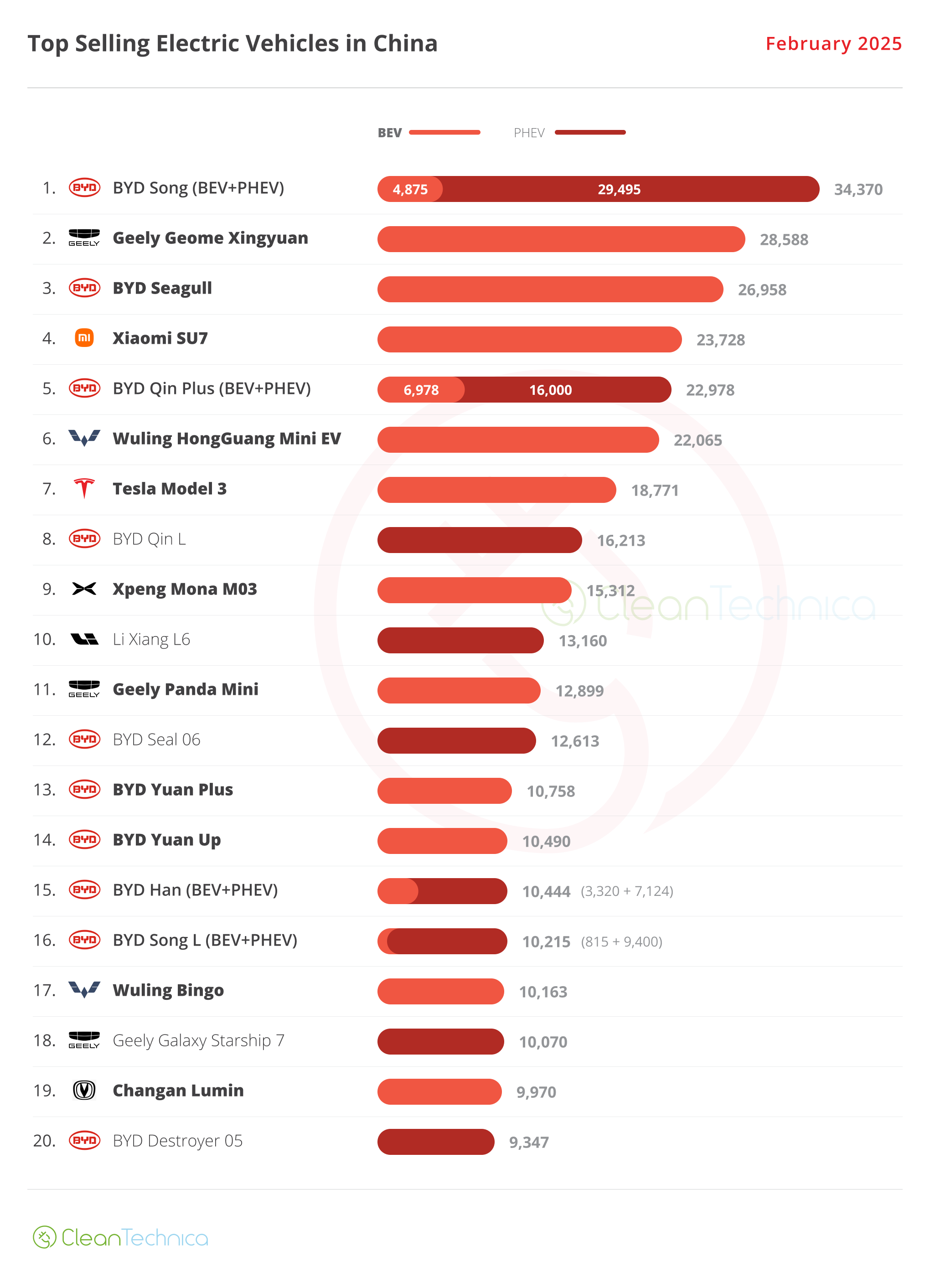

Regarding last month’s plugin best sellers table, the top 3 best selling models in the overall table exactly mirrored the ones in the EV table. After a surprisingly balanced January, BYD resumed the domination of the top 5, with three representatives. Here’s more info and commentary on February’s top selling electric models:

#1 — BYD Song (BEV+PHEV)

BYD’s midsize SUV is the uncontested leader in the Chinese automotive market, scoring 34,370 registrations, a 66% improvement YoY. Will the Song continue to rule in the Chinese automotive market? Well, it depends on the competition, including internal competitors. Also, how significant will constant improvements be, not only regarding powertrains, but also ADAS and software updates. True, price is one of its key selling points, but that alone won’t be enough in an increasingly competitive market. BYD’s midsize SUV will need constant improvements if it wants to continue clocking 40,000–50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market.

#2 — Geely Geome Xingyuan

A BYD Dolphin for BYD Seagull money. At least, that’s how Geely’s internal memo might have described the Geome Xingyuan when developing its latest hatchback. And with an interesting name, as Xingyuan translates as “wishing upon a star,” is Geely wishing on a star to take BYD’s leadership position? Well, that’s what the Xingyuan did in the B-class category last month. It obliterated BYD’s models as well as the rest of the competition (it more than doubled the sales of the #2 BYD Yuan Up). What does this hatchback have that makes it so special? Besides all the support that comes from a leading OEM like Geely, it has a rounded, sensible design, somewhere between a Wuling Bingo and a Smart #3. Starting with an 80,000 CNY (+/-$11,000) price, the buyer gets a 30 kWh LFP battery from CATL, which is nothing to write home about until you realise that its price places it closer to the BYD Seagull (70,000 CNY for the 30 kWh version) than the BYD Dolphin (100,000 CNY). In February, the Geely model hit a record 28,588 registrations.

#3 — BYD Seagull

Things continue to go well for the hatchback model, with the small EV securing another top 5 presence thanks to 26,958 registrations. With part of production now being diverted to export markets (And landing in Europe in Q2! For less than 20,000 euros! Yeeey!!!….), it seems demand for the little Lambo is now at cruising speed in China. The perky EV is now in podium territory. Even with its attention now diverted to other geographies, like Latin America, Asia-Pacific, and soon Europe, expect the little BYD to continue being part of the BYD pack that populates the Chinese top 10.

#4 — Xiaomi SU7

Veni, Vidi, Vici. “I came; I saw; I conquered.” This could have been the SU7’s motto. Having just landed in April of last year, Xiaomi’s flagship sedan has beaten nearly every demand/production record in the EV game, but I will just mention one: It took only 230 days to deliver its 100,000th unit! And even though prices start at 216,000 CNY, or around $30,000, this is no barebones, cheap EV. What you get in return is mind blowing value for money — a RWD full size sedan with a 74 kWh LFP battery from BYD, a 300 hp motor that pushes you from 0–100 km/h in 5.3 seconds, and a nice (if somewhat generic — did anyone say “Taycan”?) design made with the contribution of a certain Chris Bangle. Currently in its 10th month on the market, after winning its first top 5 presence in January, the sports sedan did even better in February, riding to 4th. Will we see it reach the podium in March? Or will we have to wait for Q2? Anyway, thanks to 23,728 registrations, it also won the full size category leadership position. And… last month, it was the best selling sedan in China, all powertrains included! With an 8–9 month waitlist in China alone, expect the sedan to be a serious candidate for the full size category leadership position in 2025, and with export plans now set in motion, expect its success story to be replicated in many markets.

#5 — BYD Qin Plus (BEV+PHEV)

Along with the Song, the BYD Qin has been a bread and butter model for the Chinese automaker for a long time. The midsizer reached 22,978 registrations in February, which is a 25% decline over the same period last month. So, it seems the midsize sedan is not holding on as well as its SUV sibling. With the price starting at 80,000 CNY ($12,000), it continues to be one of the cheapest in its category, but price alone won’t be enough to keep sales high.

Looking at the rest of the best seller table, the highlight comes from Wuling, which placed its tiny Mini EV in 6th thanks to over 22,000 registrations, a 67% surge over the same period last year. And with the 5-door version coming soon, expect it to knock on the top 5 door soon…

The Tesla Model 3 compensated for the Model Y’s slow performance (just 8,006 units, its lowest result since July 2022) with a surprising peak in deliveries (close to 19,000 units). That allowed it to get a (now rare) top 10 presence.

Another sedan liftback to shine was Xpeng’s Mona M03, which joined the top half of the table in 9th thanks to 15,312 registrations. Considering the current weakness of the EV team in the C-class category, I am rooting for the startup model to rise even further in the charts, so that we can remove those pesky ICE models from the compact category leadership platform.

BYD returned en force to the top 20, placing 10 representatives there. The highlights were the two Yuan crossovers, the compact Yuan Plus and the slightly smaller Yuan Up, with both returning to the table in February after an unexpected absence in January.

After a surprising 6th position in January, thanks to an amazing 20,000 deliveries, the Geely Starship 7 returned to a more normal 18th spot, with around 10,000 deliveries, which is still a positive result for Geely’s BYD Song killer midsize SUV.

Outside the top 20, this time there wasn’t that much to talk about, with the highlights being the solid results of the Leapmotor C10 (8,054 units) and Luxeed R7 (8,748 units), all while the Geely brand had a couple of models showing up on the radar, like the Geely Galaxy E5 (8,016 units) and the striking Geely Galaxy L6 sedan — which, thanks to a recent refresh, including a new powertrain, has managed to beat its previous sales record by scoring 6,676 registrations in February. Will this be Geely’s BYD Qin Plus fighter? More importantly, will it have a chance to reach a top 20 position?

The 20 Best Selling Electric Vehicles in China — January–February 2024

Looking at the 2025 ranking, the leading BYD Song is well above the competition, but below it, there is a lot to talk about.

Benefitting from the Tesla Model Y refresh slowdown, and the Geely Starship 7 return to normal values, there were a lot of models rising in the top positions. The Wuling Mini EV was up one spot, to 3rd, while the Xiaomi SU7 climbed one position, to 4th. Now … will the sports sedan reach the podium in March? I wouldn’t bet against it.

The other two big climbers in the top half of the table were the BYD Seagull, which after a so so January jumped three positions in February to 5th, and the Xpeng Mona M03, which was up two positions to 9th. Despite a challenging original design, Xpeng’s compact model is fulfilling high expectations, helping Xpeng to be the next Chinese startup to reach profitability.

In the second half of the table, there were no major movements, with the highlights being Li Auto’s L6 midsize SUV climbing one position to 12th while the BYD Yuan Plus returned to the table at #20.

Looking at the overall manufacturer ranking, after January’s shock move by Geely, with its 198,000 units allowing it to beat BYD, there was a lot of expectation to know what would happen in February. Would Geely be able to repeat January’s surprise, or would BYD return to its commanding position?

Well … normality won. BYD returned to the leadership spot, but despite dropping to 2nd, Geely is surging 71% YoY, so it seems Geely is here to stay and will be the only one able to fight BYD this year in the overall market.

(Well, competition is always welcome….)

#8 Honda continues to freefall, down 41% YoY, and it wouldn’t be surprising to see it kicked out of the overall top 10 sometime during Q2.

Outside this top 10, a mention goes out to Leapmotor, which is continuing to grow fast (+139% YoY). Then there’s also Xiaomi, which is already showing up in the top 20 … despite having just one model on sale.

On the losers side, Dongfeng had another horrible month and is now down 57% YoY. It’s no wonder Dongfeng is said to be bought merging with Changan…. After foreign legacy OEMs, apparently, now even Chinese legacy OEMs are starting to feel the walls closing in.

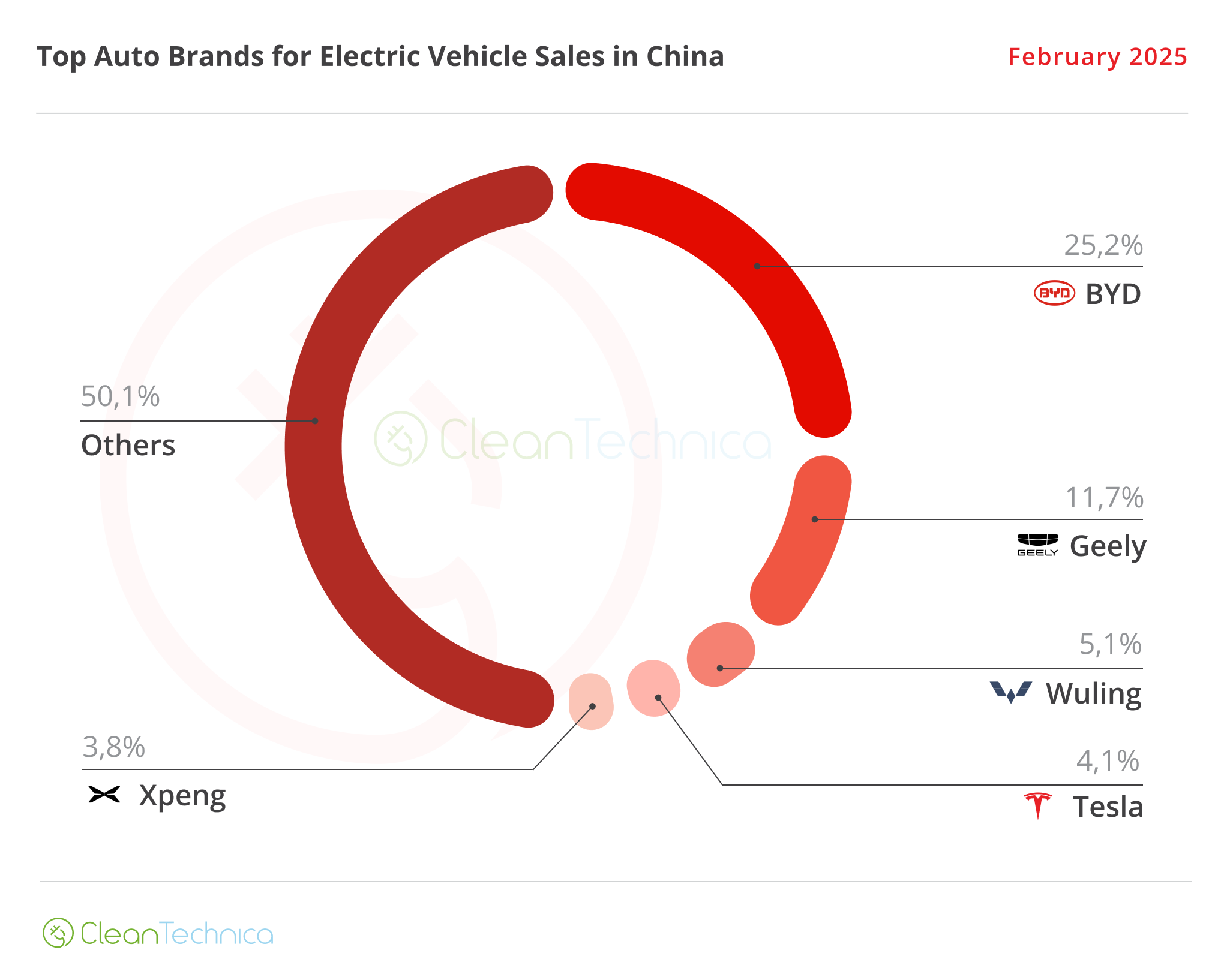

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking, there’s some news, but not at the top. BYD (25.2%, up from 24.5%) remains as stable in its leadership position as ever.

It’s the same story with Geely (11.7%, down 0.7% in February), with the brand now standing firm in the runner-up position, which is a major improvement from the 5th spot it had in the same period last year.

Things get more interesting below, though. Wuling (5.1%) is stable in the 3rd spot, while Tesla suffered from a slow month in February (4.1% now vs 4.5% in January) and is now within target range of the new #5, Xpeng (3.8%) — which just surpassed Li Auto (also 3.8% share, but some 1,000 units behind Xpeng).

Of course, Tesla is expected to have a peak month in March, which should help it move away from Xpeng and come closer to #3 Wuling, but Tesla’s current performance pales next to where it was a year ago (by then it was 2nd, with 6.2% share, versus 4th, with 3.8% share now).

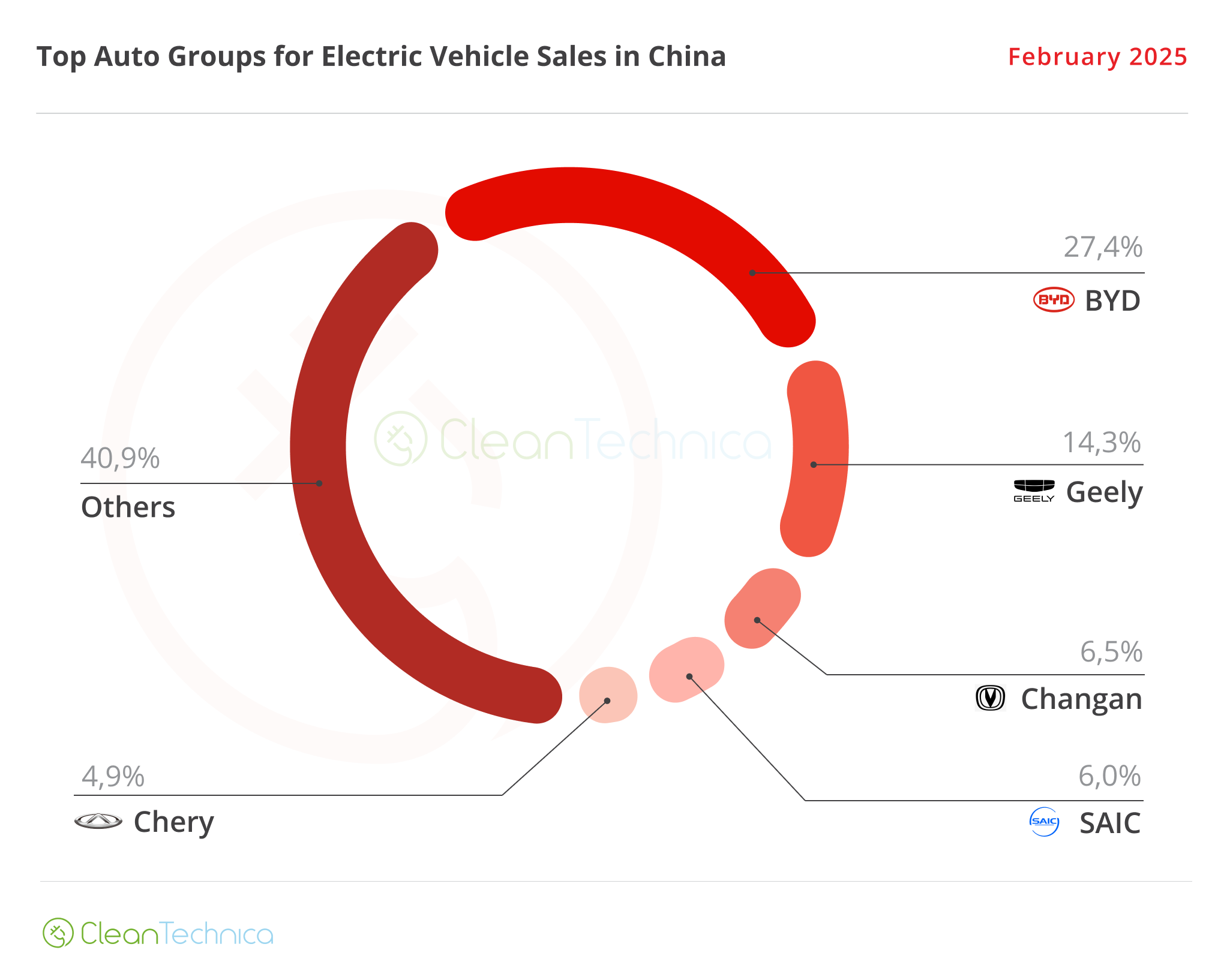

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading, with 27.4% share of the market, while Geely is a distant runner-up, with 14.3% share.

Far from runner-up Geely, #3 Changan (6.5%, down 0.4 percentage points) is keeping #4 SAIC (6%) at bay, with the Shanghai OEM not able to replicate Wuling’s success with its remaining brands.

Unlike SAIC, #5 Chery (4.9%) is benefitting from positive results across its lineup of brands, namely the premium Luxeed brand and the lifestyle iCar brand. Furthermore, it is keeping enough distance from #6 Tesla (4.1%), #7 Xpeng (3.8%), and #8 Li Auto (3.8%) to look forward to another top 5 presence in March.

Whether you have solar power or not, please complete our latest solar power survey.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy