Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

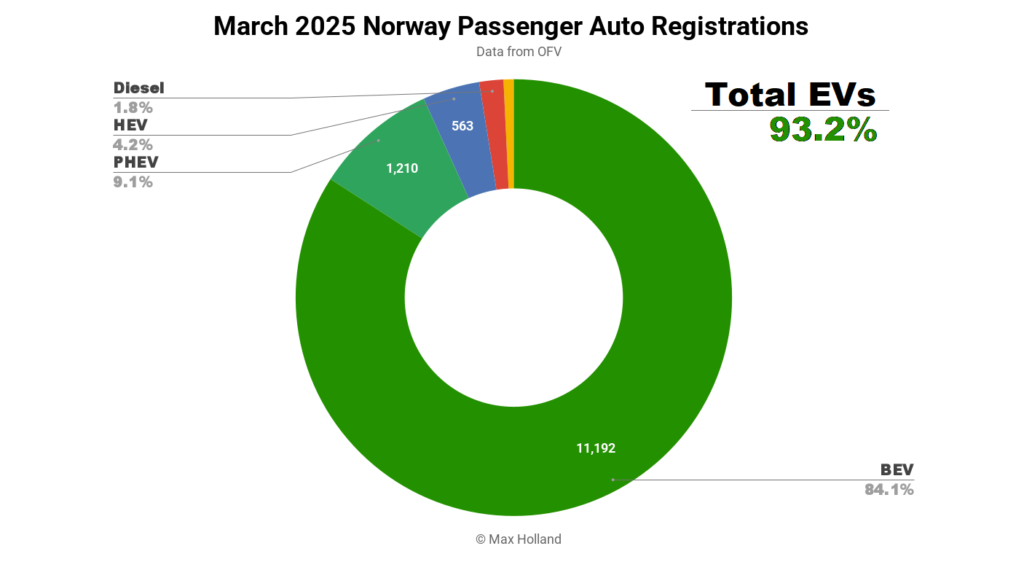

March saw plugin EVs take 93.2% share in Norway, up from 91.5% year-on-year. PHEVs saw a large pull forward ahead of an April 1st tax tightening, and thus temporarily took share from BEVs. Overall auto volume was 13,304 units, up some 36% YoY, though from a low base. The new Tesla Model Y Juniper was the best seller.

March’s auto sales saw combined EVs take 93.2% share in Norway, comprising 84.1% full electrics (BEVs), and 9.1% plugin hybrids (PHEVs). These compare with YoY figures of 91.5% combined, with 89.3% BEV, and 2.2% PHEV.

As mentioned in last month’s report, April 1st sees a significant increase in taxes on PHEVs, and thus March represented a last-chance to purchase these vehicles before that effective cost increase. They thus saw a huge pull forward, to 1,210 units, some 4.5x their trailing 12 month average. Because of this temporary distortion, BEV share took the corresponding dent. More importantly, BEV volumes were up by 28.5% year on year, to 11,192 units.

I’ve reiterated several times that Norway’s incentive policy should surely prioritise BEVs > PHEVs > HEVs > ICE. Yet, for some reason, there’s an apparent puritanical stance directed towards casting PHEVs as the significant sinners, even though diesels and HEVs (both entirely dependent on fossil fuel combustion) have each been consistently selling in higher numbers. If someone can explain this to me, I’d be grateful. Last month I ascribed it to what Weber called Gesinnungsethik, a somewhat simplistic virtue-signalling approach to morality.

Anyway, let’s see what happens with this new penalty tax on PHEVs. I suspect that – rather than the intended result of only BEVs moving into the space left over by diminished PHEV sales – in reality, both diesels and HEVs will also grow their sales a bit, to occupy the vacant market share.

Best Selling BEV Models

The new Tesla Model Y “Juniper” update started delivering in Norway in March, and has already regained the top spot in the rankings, with 1,817 units delivered. A few of the registrations were likely final inventory units of the outgoing model (there are still 44 of these listed on Tesla Norway’s “inventory” page as of early April), though I would guess that the great majority were the new Juniper.

In second position was the Volkswagen ID.Buzz, with 582 units, its biggest volume in the past year. In third was the Nissan Ariya (last month’s leader) with 553 units.

Volkswagen Group took 5 of the top 10, a decent result, with the ID.7 hitting its highest volumes yet, with 520 units, taking 5th spot.

Further back, in 15th place, the Xpeng G6 also saw its highest volumes so far, with 183 units. Just outside the top 20, the BYD Sealion, and the Audi A6 e-tron, each saw personal best volumes.

The new Hyundai Inster, which first saw decent volume in February (with 62 units), saw a steady ramp up of deliveries to 105 units in March. On this trendline, it should enter the top 20 in May or June, though much will depend on Hyundai’s shipping schedules from Korea over to Europe. This is a promising trajectory, and would seem to answer my question from last month as to whether this size of car can have broad appeal in Norway.

In the longer term, if there’s sufficient sustained demand for Inster in Europe, Hyundai may start manufacturing the Inster in their factory in Nošovice, Czech Republic.

As for March’s BEV debutants, there were three. The highest volume entry was 22 units, for the Voyah Courage, a mid-sized SUV with length of 4,725 mm, and an MSRP from NOK 419,900 (€35,600). This competes with the Tesla Model Y (from NOK 444,990), though undercutting the category leader on price by a very slight 6%. The WLTP range of the entry 2WD variant of the Courage is 445 km, and the Voyah website lists 10% to 80% DC charging in 32 minutes. These are okay technical specs, though not remarkable in 2025, and not very competitive compared to the entry Model Y’s 500 km and 24 minute charging (with the reliability of the Supercharger network).

Voyah’s other model, the “Free” only averages about 11 units per month, so let’s see if the new Courage model will have any greater success. It may be that the 22 unit debut will be its highest volume for a while to come, unless it can perhaps compete more effectively (with Tesla and others) on price. Perhaps the “street price” for the Voyah Courage will be significantly lower than the MSRP? Let us know in the comments if you have local knowledge.

The second debutant in March, with 19 initial units, was the new MG S5, a compact-mid SUV with length of 4,476 mm. For reference, this is roughly the same size as the current Kia Niro (4,420 mm), and a good bit longer than the MG ZS (4,323 mm) which rumour says it will eventually replace. The new MG S5 has not yet officially launched to customers in Norway (these 19 units are likely for test drives and showrooms) and does not yet have an official MSRP or reservations page.

We should keep an eye on the MG S5 because – like all other MG models – it will likely be very keenly priced (possibly starting close to 350,000 NOK), and have nearly 500 km WLTP range. If so, it has a decent chance to slip into the top 20, at least some of the time.

The final March debutant, with just a single unit, was the new Citroen e-C3 Aircross. This is the much larger (4,395 mm), chunkier, compact-mid SUV sibling of the regular Citroen e-C3 (3,981 mm), with a size close to that of the Kia Niro and MG S5 mentioned above.

The MSRP of the Aircross starts from 279,900 NOK (€23,750), for the 44 kWh entry version, with a WLTP range of 303 km. There was early speculation that it might come with the option of 7 seats – but I haven’t seen that confirmed in the official details yet (please let us know if you have insights).

There may later be an option for a slightly larger battery. This would open the Aircross up to many more Norwegian buyers, since the rating of 303 km will make the 44 kWh only marginally practical for long journeys in the mid-winter. In southern European temperatures, however, it’s a different story, as the 44 kWh Aircross will likely be enough for many folks, thus it does make sense as a European model.

Don’t forget that the Nissan Leaf 40 kWh has accumulated hundreds of thousands of sales over the past 7 years, and still sells decently in several markets to this day. That’s despite the 40 kWh Leaf having 10% less range, and significantly slower charging (especially after the first DC charge) than this 44 kWh Citroen e-C3 Aircross. Not everyone needs their car to be a roadtrip maestro. Let’s keep an eye on the Aircross.

Here’s the check-up on the 3-month rankings:

With the decent March performance, the Tesla Model Y remained at the top of the trailing 3-month chart. The Toyota BZ4X took second, with the Nissan Ariya in third (though only fractionally ahead of the Volkswagen ID.4).

The notable progress continues for the Kia EV3, which only saw its debut in November, and thus didn’t feature in the top 20 three months ago. Since then it has climbed steadily, to 24th in January’s trailing 3-months, then 18th in February, and now to 11th spot in the March chart. This is already a great result, though I expect it will be a frequent visitor into the top 10 in the future.

It is possible to see the new Hyundai Inster making it into the top 20 in a few months from now, if demand is sustained and the supply is there. Let’s keep an eye out for that.

Outlook

The nominal March uptick in YoY auto volumes came from a low base, with Q1 2025 overall slightly down on seasonal norms. The broader Norwegian economy saw a downtick in the latest macro data, with 2024 Q4 showing negative -0.3% GDP year-on-year.

However, erratic quarterly GDP figures are fairly normal for tiny Norway, heavily dependent as it is on fossil fuel export receipts. Inflation saw an uptick to 3.6% in February (latest data), from 2.3% in January. Interest rates remained flat at 4.5% in March, unchanged since December 2023. Manufacturing PMI was at 50.6 points in March, down from 51.9 points in February.

Let’s see what happens in the coming few months to PHEV sales, compared to the other residual powertrains. With ever simpler and more affordable BEV models coming available, the EV transition in Norway will no doubt continue, and it is interesting to watch the dynamics of the late-phase adoption curve play out.

What are your thoughts on Norway’s auto market? What models are you looking out for? Please share your thoughts in the comments below.

Whether you have solar power or not, please complete our latest solar power survey.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy