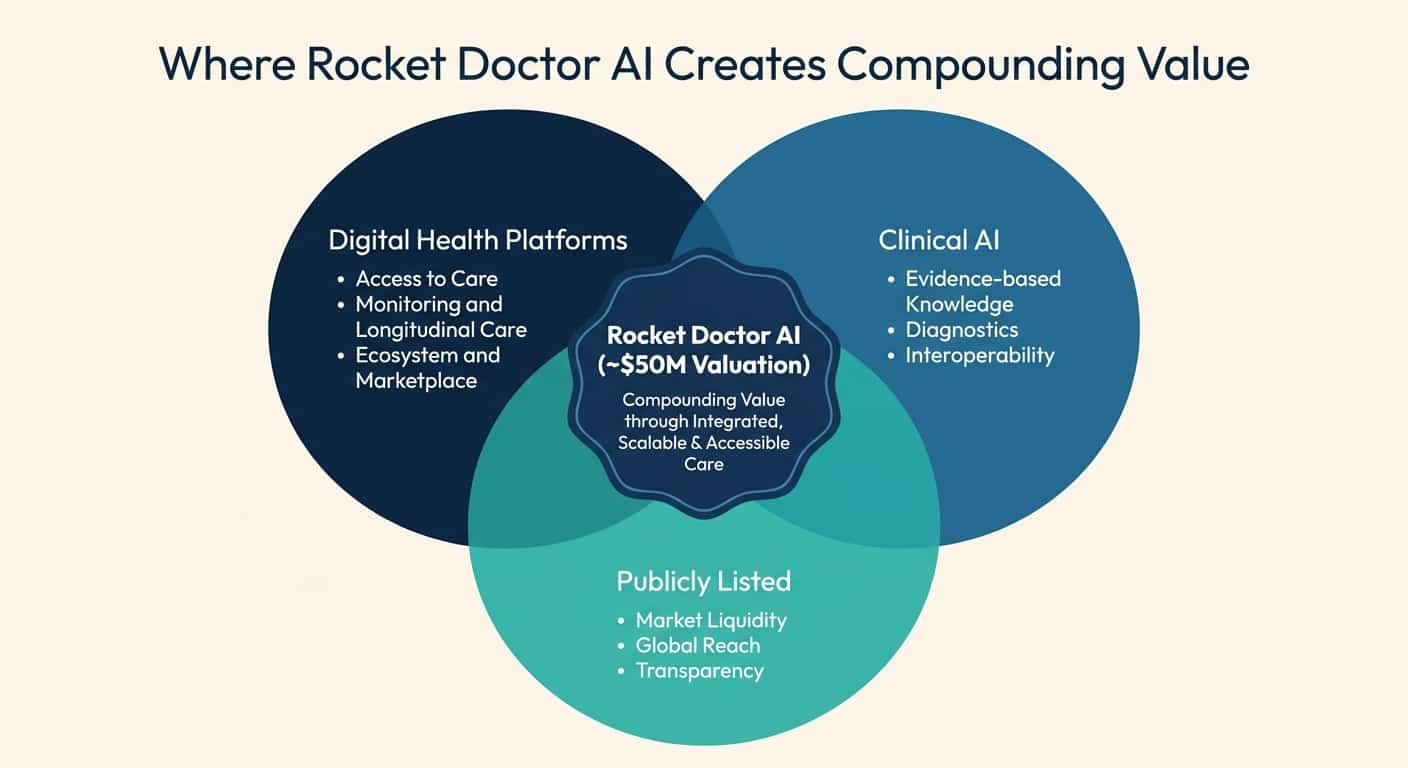

Two Integrated Assets in One Company

Rocket Doctor AI operates two interconnected businesses: a revenue-generating virtual care platform and a proprietary clinical AI engine.

Source: Company materials and public filings

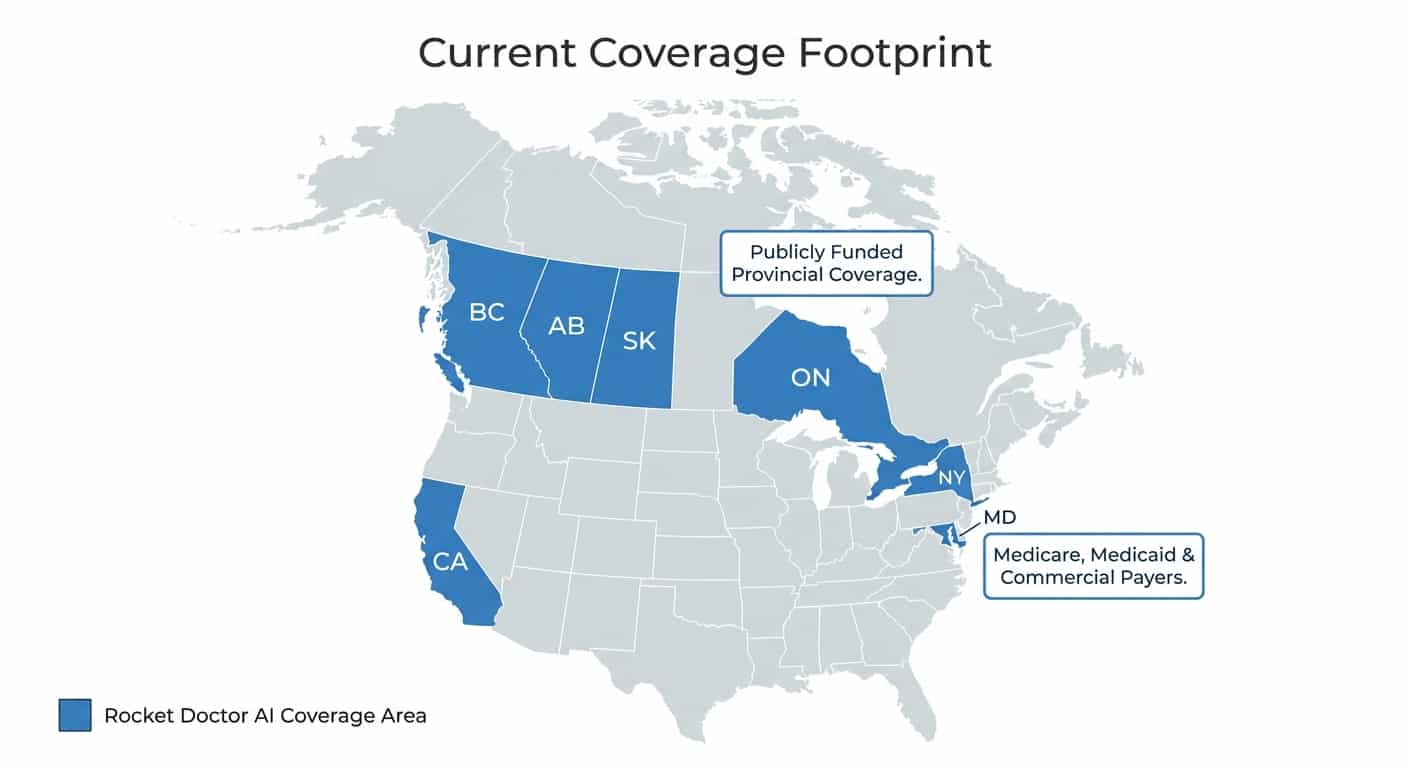

Rocket Doctor — The Virtual Care Platform

A digital health marketplace enabling 300+ physicians to independently launch and manage virtual or hybrid practices. 700,000+ patient visits across four Canadian provinces and three U.S. states. In-network with payers covering over 13 million lives including Medicaid, Medicare Advantage, VA, and commercial plans.

Global Library of Medicine (GLM)

A physician-curated clinical decision support system developed over 9 years with input from hundreds of physicians. Covers 1,000+ diseases and 17,000+ symptoms. Uses structured, validated clinical data with audit trails — designed to triage, diagnose differentially, and adjust recommendations as new patient data is entered.

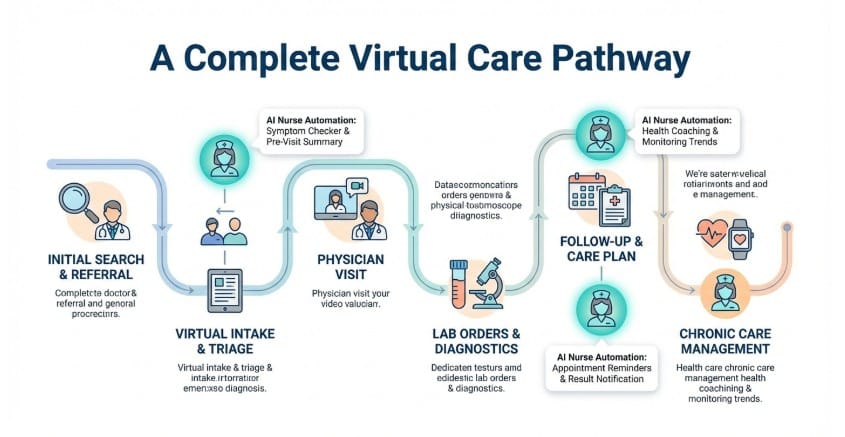

A Complete Virtual Care Pathway

The platform supports the full patient journey — from initial search and curated AI powered triage through physician visit, lab orders, follow-up, and chronic care management.

Source: Company materials

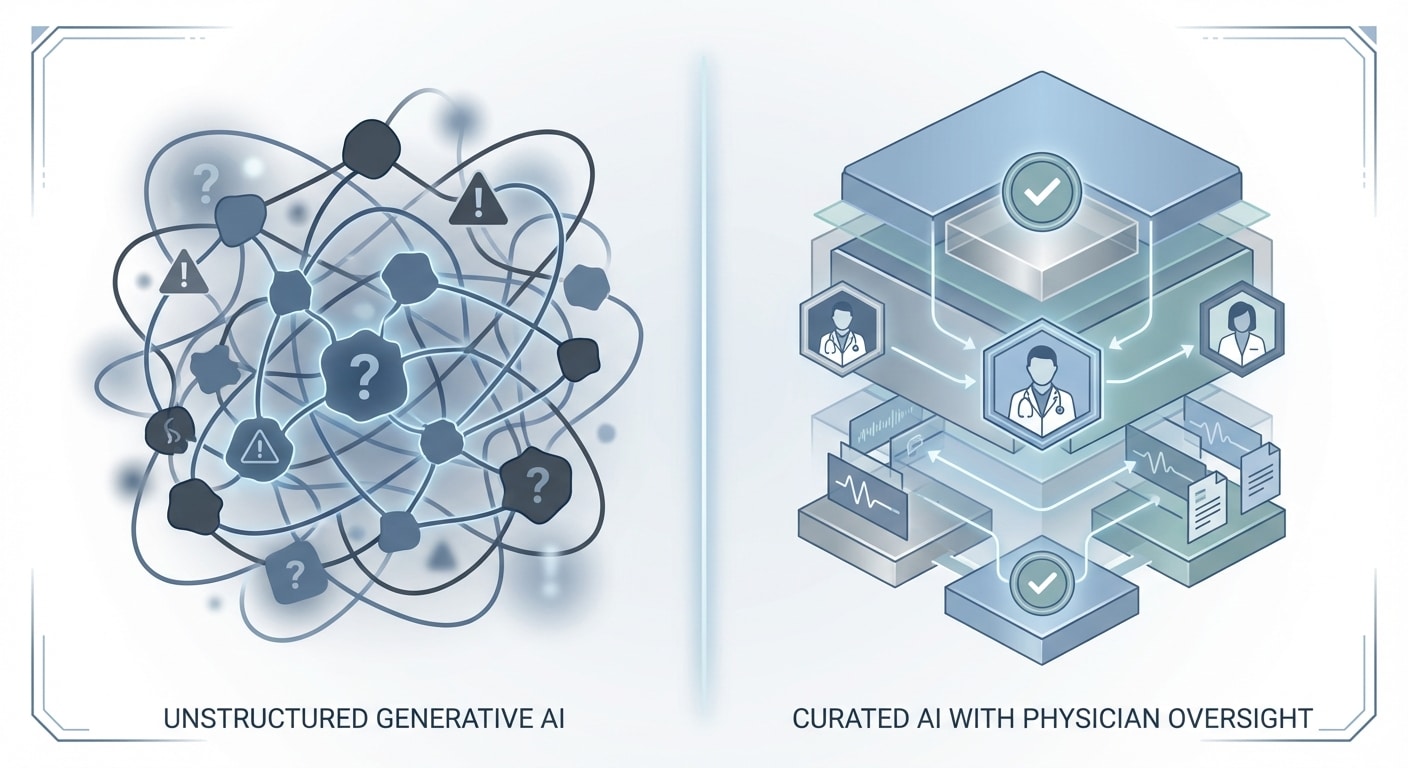

Curated Clinical AI vs. Generative AI

Management has highlighted key areas where the Global Library of Medicine is designed to differ from generative AI approaches.

Source: Company materials and industry comparison

Curated, Not Generative

Content built through structured development and physician-led review. Every data point is physician-validated with full audit trails.

Dynamic Differential Diagnosis

The platform recalculates diagnoses as new patient details emerge — including lab results and imaging — adjusting the differential in real time.

Multiple Deployment Options

Powers chatbots, voice assistants, and avatars. Designed for white-labeling, multilingual deployment, and EMR/telehealth integration behind client firewalls.

Supporting Next Generation Medical Education

A non-medical undergraduate using the system correctly diagnosed 11 of 12 patients in a medical school-level exam — 92% vs. a typical passing threshold of 60–70%.

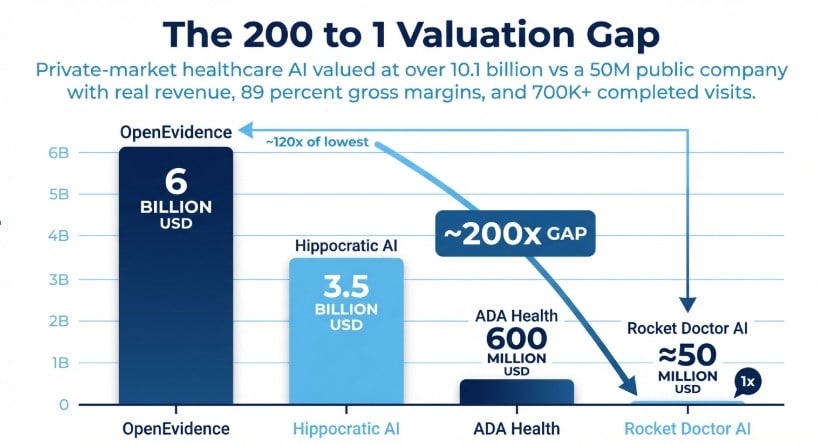

The Healthcare AI Landscape

A comparison of public and private healthcare AI company valuations, based on publicly available data. Valuations are approximate and sourced from company disclosures and reported funding rounds.

Competitor valuations based on most recently reported funding rounds. Not a recommendation to buy or sell any security.